Quick answer: yes, you can invest in US stocks from India without an Indian demat account. US stocks are held in a US brokerage account, not in an Indian demat. Your Indian demat account is only for Indian securities, it has nothing to do with Apple, Tesla or the S&P 500.

This confuses a lot of first-time investors, so let us clear it up properly and then walk through exactly how to start, what it costs, and the tax rules nobody tells you about until it is too late.

Why You Do Not Need a Demat Account for US Stocks

In India, shares are stored in dematerialised form with NSDL or CDSL, and your demat account is the locker. The US system works differently. When you buy US stocks, they sit with a US broker-dealer, and your ownership is protected by SIPC insurance up to $500,000 (including $250,000 for cash) if the broker fails.

So when an app says “invest in US stocks, no demat needed,” it is not a loophole or a trick. That is simply how the US market works for everyone.

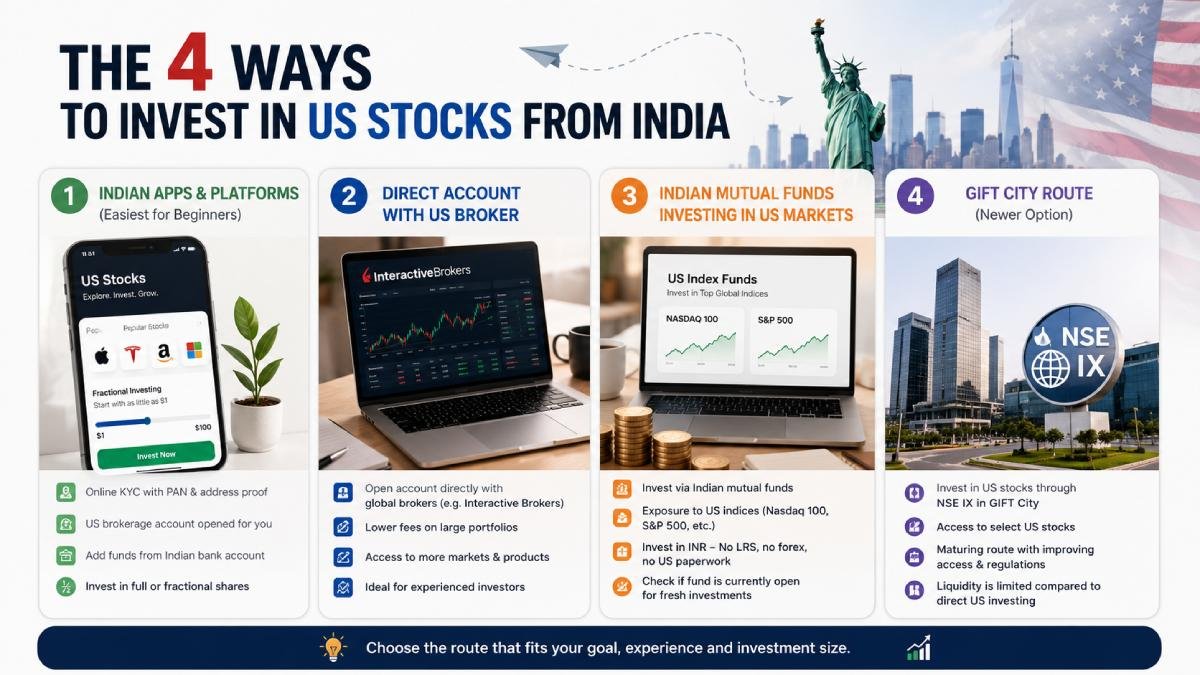

The 4 Ways to Invest in US Stocks from India

1. Indian Apps and Platforms (Easiest for Beginners)

Platforms like INDmoney, Vested, Appreciate and Groww’s US stocks offering partner with US brokers to open an account in your name. The process is fully online:

- Complete KYC with PAN and address proof

- The platform opens a US brokerage account for you with their partner broker

- Add funds from your Indian bank account

- Buy full or fractional shares

Fractional investing is a big plus here. You do not need $200 plus for one Apple share, you can start with as little as $1.

2. Direct Account with a US Broker

Brokers like Interactive Brokers accept Indian residents directly. This route gives you lower charges on large portfolios and access to more markets, but the interface is built for experienced traders and the account opening asks for more documentation. If you plan to invest serious money (above Rs 10-15 lakh), this route usually works out cheaper long term.

3. Indian Mutual Funds That Invest in US Markets

If sending money abroad feels like too much work, Indian fund houses run schemes that invest in US indices like the Nasdaq 100 or S&P 500. You invest in rupees through your normal mutual fund account. No LRS, no forex, no US paperwork. One catch: these funds sometimes pause fresh investments when the industry-wide overseas investment limit gets hit, so check if the fund is currently accepting money.

4. GIFT City Route (Newer Option)

Through NSE IX in GIFT City, Indian investors can access select US stocks. It is still maturing, liquidity is limited compared to direct US investing, but worth knowing it exists because rules and access keep improving every year.

How the Money Actually Goes: LRS Explained

All direct foreign investing happens under RBI’s Liberalised Remittance Scheme (LRS). Key rules for 2026:

- You can remit up to $250,000 per financial year per person

- TCS (tax collected at source) of 20% applies on amounts above Rs 10 lakh in a financial year for investments. Below Rs 10 lakh, no TCS

- TCS is not an extra tax. You claim it back as credit when filing your ITR, it just blocks your cash flow for a while

Most beginners investing Rs 1-5 lakh a year never touch the TCS limit, so do not let that scare you.

What It Costs: The Charges That Actually Matter

| Charge | Typical Range |

|---|---|

| Forex conversion (INR to USD) | 0.5% to 2% of amount |

| Brokerage per trade | Zero to $2 on most apps |

| Withdrawal back to India | $5 to $35 flat |

| Annual account fee | Mostly zero |

The forex spread is the silent killer, not brokerage. A platform advertising “zero brokerage” but charging 1.5% on currency conversion is more expensive than one charging $1 per trade with a 0.5% forex rate. Always compare the conversion rate before picking a platform.

Tax on US Stocks for Indian Residents

This part is important, so read it twice.

Dividends: The US deducts 25% tax at source (thanks to the India-US tax treaty, it is 25% instead of 30%). The dividend is then also taxable in India at your slab rate, but you claim credit for the 25% already paid using Form 67 with your ITR. No double taxation, just paperwork.

Capital gains: The US does not tax your capital gains as a foreign investor. India does:

- Held more than 24 months: long term capital gains at 12.5% (plus surcharge and cess)

- Held 24 months or less: short term, taxed at your income slab rate

Disclosure: You must report foreign assets in Schedule FA of your ITR every year you hold US stocks, even if you sold nothing and earned nothing. Missing Schedule FA can attract penalties under the Black Money Act, and they are harsh. This is the single most ignored rule among new US stock investors from India.

Which Route Should You Pick?

- Just starting, small amounts: Indian app with fractional shares. Low friction, start with $50 if you want

- Want zero paperwork: Indian mutual funds investing in US indices

- Serious long-term portfolio: Direct account with an international broker for lower total costs

- Only want index exposure: S&P 500 or Nasdaq 100 ETFs through any of the above, honestly the sensible choice for most people

Frequently Asked Questions

Is it legal to buy US stocks from India?

Completely legal. RBI’s LRS framework explicitly permits it. Millions of Indians already do it.

Do I need a US bank account or SSN?

No. Your Indian bank account and PAN are enough. The platform handles the US side with a W-8BEN form, which they fill for you digitally.

Can NRIs use these Indian platforms?

Mostly no. These platforms are built for Indian residents under LRS. NRIs in the USA should just open a regular US brokerage account directly, it is simpler and cheaper for them.

What happens to my stocks if the app shuts down?

Your stocks are held with the US broker in your name, not with the Indian app. SIPC protection covers up to $500,000. You would transfer your holdings to another broker.

How much money do I need to start?

As little as Rs 100-500 on platforms offering fractional shares. Though realistically, keep forex and withdrawal charges in mind, investing at least a few thousand rupees at a time keeps costs proportionate.